I was wondering back in 2017 how what I was taught about economics applies to a nation. I wrote then I read, all too often, that economic theory says that the nation state is different from the domestic position. This particularly applies to borrowing. I could not have bought my first house without credit, but the cost of that credit was so much that I worked hard to reduce that borrowing, having it well under control in 1990 and have been completely free of borrowing of any sort (I pay off my credit card every month) since 1997. I can no longer conceive of a position in which I would want to borrow money, but at the same time I am aware that, having a sell-by date of under 30 years, I’m not in a position to petition for credit and that a nation state is not in such a position (since very few disappear / die).

I am told that Keynesian thinking says a state should borrow when the economy is slow (whatever that means) and pay it off when the economy is good. That implies there is a line above which one pays off and below which one borrows – it may be a region, and it may depend on the position of other competing states. That is a statement of theory, unsupported by argument but no doubt I could find it. Is it an accepted truth and, if it was one, is it still?

Let's see if this can be clarified, at least enough to make clear the precise questions that need to be answered.

A nation such as Britain prints its currency and claims that this money is backed by gold. I don't think there is enough gold to match the amount of money in circulation; if the pound has to be backed by gold then the total currency in circulation is fixed by the amount of gold, which must have a limit. A government spends money and collects taxes and generally the difference of spend-taxes is called deficit. This term suggests that a deficit is bad, but that implies that the domestic model above applies. But it doesn't apply because the domestic environment is very different to that of a state government. Particularly, at a domestic level there is a fixed amount of money and if spend exceeds the money supply then eventually one goes bankrupt. Does the same apply to a nation? I am uncertain, and it appears that perhaps this is not so. A sovereign nation doesn't run out of money because it simply prints more of it – and in practice it doesn't even need to do that, it simply appears by magic, electronically. Meanwhile the accounting processes say that the deficit has grown.

In order to prevent various disasters such as runaway inflation, the government sells its debt indirectly to the central bank (the Bank of England). The government sells bonds in its own name—treasuries, government bonds—which are purchased by the central bank, other banks and investors In the same way, central banks buy bonds from other sources, especially from other banks. This allows there to be more (or less) money in the economy. In the current environment, we're interested in there being more money, because we would like to spend vast amounts on the issues raised in Essay 323.

So one relevant question is whether the household model of the national economy is wrong. Specifically if I take out a loan, I have to pay it back. If the nation takes out a loan from somewhere, does it too?

Whether this works is unclear. it increases the prices of things such as shares and property. This tends to benefit wealthier members of society who already own these things, as the Bank itself concluded in 2012. Meanwhile, younger people found it harder to buy their first homes and build up savings. Another important side effect of QE hit pension funds. Government bond prices are used to estimate how much it will cost to provide pensions in the future. If those bond prices go up, the cost of providing future pensions rises. As a result many firms were obliged to make bigger payments into their pension schemes, reducing money available to invest elsewhere. And in many cases, QE will have contributed to the decision to close pension schemes altogether. [2]. I was struck that the balance between the income and wealth effects from QE depends on the distribution of assets across household, which in turn means that in practice, the benefits from these wealth effects will accrue to those households holding most financial assets which includes pension provisions. For context, [3, §22] estimated that the 2009-2012 purchase of assets increased household wealth by an extraordinary £B600, amounting to £10k per person if evenly distributed. Which of course it is not; the rich hold far more of these assets and gain accordingly. The top 5% of households hold 40% of these assets. [3, §51]

Introduce MMT, Modern Monetary Theory [6,8]. It doesn't make sense that, if the UK is one of the richest countries, it does not have enough money (assets) to afford the things we want to do. But then we may remember that UK.gov is the 'sole issuer of the pound'. The theory says money is not a commodity like gold, whose supply is limited. So UK.gov and its agents can issue money. One wonders just how many currency issuers there are and whether there is a point at which the currency is so strong that one can indeed just decide to have more of it. ¹ There is an assumption that the government cannot default ². So if that is so, why pay taxes at all? Because tax is used to move money from those with a lot of it towards those without. Also, because we can only pay our taxes in the national currency, this creates and perpetuates a demand for that currency. It is the assumption of demand that keeps the currency viable. Government can spend, which puts into circulation the money we need with which to pay our taxes. Taxes take money out of the circulation system, but they are not the only route for money to move out of the system. For there to be a deficit, gov't spending exceeds taxes (or supply), but that difference must have gone somewhere, probably into what I think of as savings - the money taken out of the system by us the people. So that's what you have in the bank, plus your savings like ISAs and pension funds - and commercial equivalents, of course. So in a sense the mounting national deficit is also that money which has been taken out of the system and is currently being held by us. Probably unevenly, but held by us. So modern Monetary Theory asks whether settling the deficit (and here deficit is taken to be some sort of debt) means that the money we have been holding individually must be returned to the government. That does not sound like a good thing.

There must be a point at which too much money has been put into the economy, and I think that point is reached when what it wants to buy is not available (which pushes prices up and is called inflation). In a sense taxes help control inflation and inflationary tendencies. ³ Modern monetary theory very sensibly says that there needs to be the right amount of money in circulation for it to operate effectively. If businesses are running up debt, then there needs to be an adjustment that gives them surpluses which which to pay that off – and for there to be surplus with which to pay off debt, then the state must run at a deficit so as to make that money available. So this general idea says that inflation ought to be very low and that things are adjusted by the supply of money. Too little money means we have underemployed resources (people especially), too much and we have inflation, we devalue the money itself because we're at capacity for the supply of resources. Which has consequences with the neighbours, surely.

One of the issues that is political here is that MMT is what we might call 'big state' economics. That runs directly counter to Conservative party thinking, of the smallest possible state. They talk principally about state intervention but I think one begets the other.

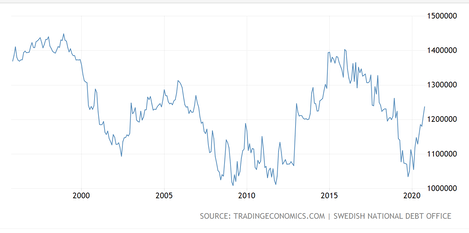

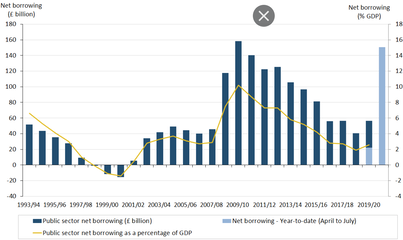

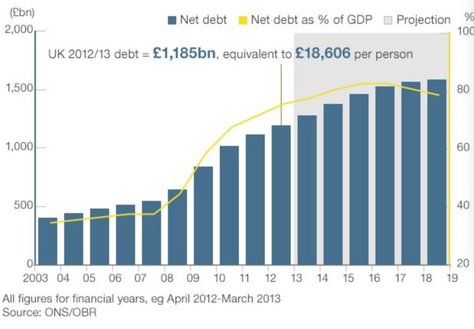

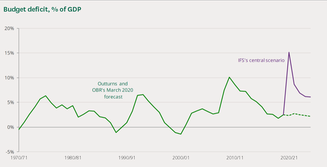

. Deficit is spending minus taxes. Budget deficit is then when intended everyday spending (what goes in the Budget) exceeds taxes, so these two are different, by the magnitude of the capital spending that occurs (think infrastructure projects). Then there's the term structural deficit which is the deficit you recognise adjusted to recognise that the economy moves in cycles. National Debt ought to be the cumulative deficit figure. I think MMT says that this too is not a bad thing. To convince yourself of this, look at the cumulative deficit for Scandinavian countries, those we look at and envy their standard of living.

The short version is that that bad-sounding thing, the deficit, need not be viewed as a bad thing at all.

DJS 20201117

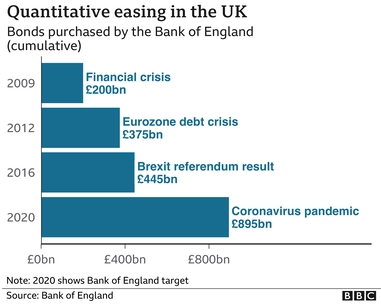

I've called this QE3 after the ships Queen Elizabeth and the QE2. If there was a next one, it would be QE3. This term was used for the 3rd round of easing from the Federal reserve, Sep 2012. The picture is of Cunard's MS Queen Elizabeth, which replaced the outgoing QE2. The reason the QE2 (69-08, since then in Dubai) was so named was because the original (39-72) was still in service.

¹ ² ³ ⁴ ⁵ ⁶ ⁷ ⁸ ⁹

1. Big ones are the USA federal bank, the European Bank, the Bank of Japan, the Bank of England, - so that's the dollar, Euro, Yen and pound. The problem isn't can you create a currency, it is that your currency is accepted.

2. Look at [9] for a list of currencies that did default. I suspect that each of these was not a currency with enough support to keep it viable.

3. Distinction between monetary and fiscal policies: Monetary policy refers to the actions of central banks to achieve macroeconomic policy objectives such as price stability, full employment, and stable economic growth. Fiscal policy refers to the tax and spending policies of the federal government. Source. So monetary policy belongs with banks, fiscal policy with government.

4. I see and hear deficit and debt used interchangeably. https://www.bbc.co.uk/news/business-25944653 The national debt is obviously what is owed. What is referred to is the net debt, being total debt less liquid assets.

[1] https://www.weforum.org/agenda/2014/11/a-beginners-guide-to-quantitative-easing/

[2] https://www.bbc.co.uk/news/business-15198789 The Bank of England is in charge of the UK's money supply - how much money is in circulation in the economy. That means it can create new money electronically. That's why QE is sometimes described as "printing money", but in fact no new physical bank notes are created. The Bank spends most of this money buying government bonds. Government bonds are a type of investment where you lend money to the government. In return, it promises to pay back a certain sum of money in the future, as well as interest in the meantime. Buying billions of pounds' worth of bonds pushes the price up: when demand for anything increases, the price usually goes up too. Many interest rates on loans offered by banks to businesses and individuals are affected by the price of government bonds. If those government bond prices go up, the interest rates on those loans should go down - making it easier for people to borrow and spend money.

[3] https://www.bankofengland.co.uk/-/media/boe/files/news/2012/july/the-distributional-effects-of-asset-purchases-paper Economists should have read this already. Read the summary, which is the first two pages. I found the whole thing largely impenetrable. It's in English, but not as I know it.

[4] https://www.youtube.com/watch?v=R0uJgbR8d-Y for those who dislike reading. Turn sound off. https://www.youtube.com/watch?v=4TihoBfdCe8 is slightly less lowbrow. My takeaway {at 1:30} was that the QE in the EU across 2012 made little difference to the total money in circulation, suggesting that without QE there would have been a great shrinkage of the economy.

[5] https://www.taxresearch.org.uk/Blog/2020/08/12/mmt-a-uk-primer/?fbclid=IwAR3ZVy_WMoykKIM2z436H71qiVgMEc0IlvbV63XDfvXwP5W72YfQSn26x1U This is Modern Monetary Theory, not QE. Points: we are one of the richest countries so it doesn't make sense that we think we don't have enough money for the things we want to do.

[7] http://www.levyinstitute.org/pubs/Wray_Understanding_Modern.pdf

[8] https://gimms.org.uk/2019/03/29/markets-are-not-in-charge/

- A government which is a sovereign currency issuer like the UK cannot run out of ‘fiscal fire power’. The IMF’s claim that the public debt is so large as to constrain future spending to deal with future recessions is quite simply a falsehood. What will constrain the spending of any government, however, are the resources it has at its disposal. Its public policy choices define their distribution, how they will be used and in whose interests. A government’s economic record must be judged, not on its monetary discipline, but whether it served public purpose and created economic and social well-being. There is no other measurement.

- A currency-issuing government like the UK doesn’t have to issue debt in order to cover its deficit and the bond markets can never bankrupt such a nation. When the government sells bonds, it can always service those liabilities provided they are denominated in its own currency. As Professor Bill Mitchell says, ‘The bond markets are supplicants not a source of spending capacity’.

- The spending of a government like the UK which is a sovereign currency issuer is not constrained by its ability to collect tax. In other words, it is not like a household budget which needs income before it can spend. Whilst it is a good idea to review global corporate tax rules as a mechanism to redistribute wealth and resources more fairly Christine Lagarde’s claim that doing so will allow governments to spend on public services is just a part of the same orthodox narrative which prevails and is incorrect.

[9] A contrary view. https://www.dlacalle.com/en/no-governments-with-monetary-sovereignty-cannot-issue-all-the-debt-they-want/

[10] Another such dampener. https://iea.org.uk/beware-the-siren-call-of-modern-monetary-theory/ It deserves a critique; essay project (for you, not me).

1. The cost of government borrowing does not depend solely on the risk of default. It also depends on expectations for inflation and exchange rates (the domestic and international value of the currency in which debts will be paid), as well as the opportunity cost of diverting resources from the private sector.

2. If the government spends so much that the total demand for goods and services exceeds the capacity of the economy to supply them, the result will be higher inflation. Again, this is pretty standard stuff. Where MMTers differ is on the appropriate policy response. More orthodox economists would see this kind of overheating as something to be tackled by monetary policy. But most MMTers would argue that the natural rate of interest is zero, or at least that central banks should set official interest rates close to zero indefinitely. Instead, in the topsy-turvy world of MMT, ‘well-targeted taxes’ should be used to control inflation by managing private demand. Many MMTers are also keen on wage and price controls, and rationing, despite the miserable track record of these forms of state intervention.

3. MMTers argue that government deficits play a crucial role in balancing the economy and are therefore essential, rather than something to fear. The key point here is that deficits and surpluses have to balance out. If the private sector needs to run a surplus to repay debts that have become unsustainably high, then the government has to run a deficit. What’s more, instead of public spending being financed by taxes, either now or in the future, MMTers claim that all public spending is in fact paid for (in some way) by the creation of money. Some go even further and argue that government deficits provide the additional money required to support economic growth. However, it is simply not right to say that budget deficits are necessary for a successful economy. Many countries, notably in Scandinavia, have run budget surpluses for long periods in the past and still enjoyed sustained increases in living standards. In addition, deficits are usually financed by conventional borrowing, not money printing. This is true even now during the pandemic. Central banks have been buying more government bonds from private investors as part of their programmes of quantitative easing (QE), but direct monetary financing of deficits is (mostly) still taboo.

[11] https://www.bbc.co.uk/news/business-25944653 on the difference in terminology. Helpful and not, at the same time.

[12] https://commonslibrary.parliament.uk/research-briefings/sn06167/ Much better, but it should be.

Interest payments on borrowing are a significant part of government expenditure. Interest is paid on all outstanding government debt, accumulated over many years. In 2019/20, gross debt interest payments were £48 billion; net debt interest payments were £37 billion. The lower net interest figure includes the impact that the Bank of England’s quantitative easing has on the government’s debt interest payments. The Bank has bought government debt from private investors such as pension funds and insurance companies largely to get money into the economy. As some of the government’s debt is being held by another public sector body – the Bank of England – it means that when the government comes to make interest payments it is giving these payments to another part of the public sector. The net effect is that these debt interest payments are cancelled out for the public sector.