'Rent is just throwing money away'. Discuss.

What you buy with rent is the use of a space. The modes of rent do not matter much here; whether your rent includes some bills or not is part of the detail. What is at issue is how much space you have use of, at what quality and how that space serves your needs.

The implication of an alternative is to not-rent. If one then considers this opposite to be ownership, as opposed to versions of squatting or theft, then again the question has to be what it is one is buying. Buying a living space has the same constraints of what can be afforded. The perceived carrot is that of subsequent ownership. In order for ownership to occur, the mortgage (money borrowing) has to be paid off, and even if one moves house that previous loan has to be paid off.

The significant factor that supports the contention that ownership is 'better' than renting is that the growth of house prices has exceeded inflation for most of our lives. Figures from the Office for National Statistics showed the average house price across the UK increased by £31,000 to £266,000 over the past year – or just over £2,500 a month. House price inflation using Land Registry data stood at 2% in June 2020 but has gradually increased over the previous 12 months. [1]

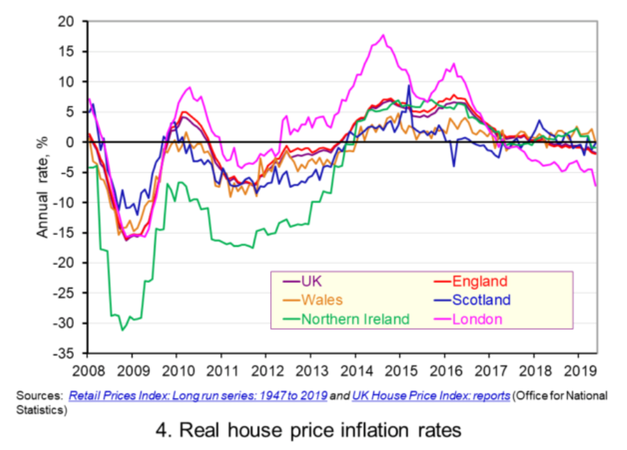

House price index does not grow evenly across a nation, which goes some way to justify the mantra 'location, location'. It does not grow evenly across quite small areas. As source [2] and the chart I have copied explain, there are occasions where house prices fall. In the year to May 2019 prices in NE England fell by 0.7 percent, while they rose in most of the rest of the UK. This same graph demonstrates the volatility of price, by charting the house price inflation rate, not price alone.

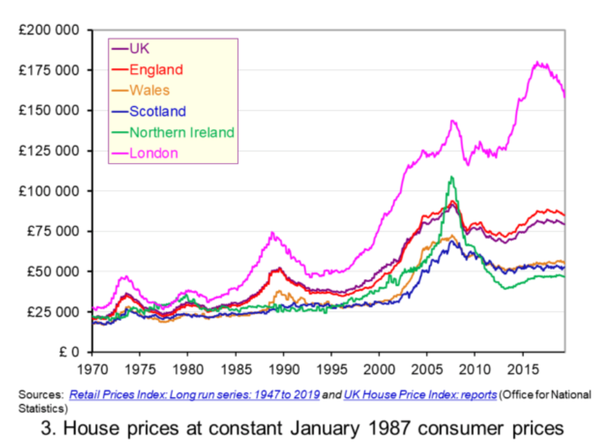

For the purposes of comparing helpfully with money inflation, we have use for a standardisation, such as the next chart, which takes Jan 1987 as a fixed point. So this third chart shows the growth in the price of housing relative to that of consumer product prices.

Over the period from January 1970 to May 2019, the average annual rate of real house price inflation was 3.2 per cent. Hence house prices have, on average, grown at an annual rate of consumer price inflation plus 3.2 per cent.

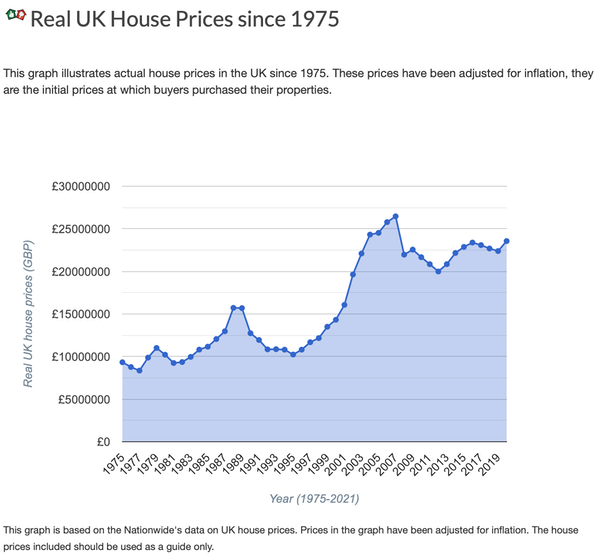

Owning a house means you hold some equity in the property, an amount of capital. Suppose you bought in 1995 at £100k with an 80% mortgage; you have invested £20k of savings (however acquired) in your house. You've been lucky, and the grey-blue chart next on the right [5] shows that in 2005 your house was worth £240k. Your mortgage will have gone down a little in that time, but most of what you have paid out is interest on the loan and the mortgage company still has about £70k equity in your house. But the other £180k is yours. So at an individual level your £20k has become £180k a growth factor of nine across ten years, which is equivalent to an investment returning almost 25% a year every year.

Source 3, takeaways

Both renting and buying have their financial advantages, and owning a home isn’t right for everyone.

Unlike homeowners, renters have no maintenance costs or repair bills and they don't have to pay property taxes.

Amenities that are generally free for renters aren't for homeowners, who have to pay for installation and maintenance.

Renting usually requires a security deposit equal to one month’s rent, whereas a homebuyer is required to have a sizable down payment when purchasing a home with a mortgage.

Renters have lower utility bills, greater flexibility in where they live, and access to amenities, such as a pool or fitness room, that might otherwise be prohibitively expensive. [3]

During this time the house owner has, we hope, done maintenance so that the house is in an equivalent state to when it was purchased, or better. If better, then some (not all) of that money spent on improvement may be recovered on sale. That rather depends on a range of very variable factors, perhaps best described as depending on who is in the market for your property at the moment you want to sell.

Takeaways, source [4]

Renting offers flexibility, predictable monthly expenses, and someone to handle repairs.

Homeownership brings intangible benefits. They include a sense of stability, belonging to a community, and pride of ownership, along with the tangible ones of tax deductions and equity.

Contrary to popular belief, renting doesn't mean you’re "throwing away money" every month, and owning doesn't always build wealth "in the long run."

This ownership thing has connotations of stability, or permanence, of belonging to not only the property but the locality, and this all adds up to a certain sort of pleasure, to which one could attach value. The big difference from the perspective of the renter is that change in capital (equity) held. Whether or not that equity has any use depends on other factors, but if income has risen such that a larger mortgage can be afforded, or a similar house with a lower mortgage or a house with more opportunity for improvement, then this can be seen externally as something lacking from the renters' position.

Rather than me trot out positives and negatives, look at the text box with takeaways from [3, 10 reasons to rent] and [4, not to]. For more detail, follow the links.

There is a perception that houses will always increase in value and, while across a long period that is generally true, it is often not true in the shorter term. Between 1991 and 1993 house values dropped by a third. I remember well some friends in the mid-1970s whose property went into negative equity, which is what happens when your house drops in value below the mortgage you are struggling to pay. That can force a sale and all the subsequent losses. Life lesson: don't go for too big a mortgage.

If you attempt to compare house ownership with other equity such as shares, you must factor into your calculations what you spend on the house to keep it at market value. Conversely, you should accept that a lack of maintenance will have consequences at sale. Similarly, it would be wrong to assume that the cost of an improvement is the same as the value added to the house. Potential owners may not like your change, which then restricts the market to whom you are selling and that is reflected in the price you eventually agree. I've written at length on some of these topics (218-solar panels, 220-bathrooms and 221-House prices for example) and I'm not going to repeat that content. My feeling is that money spent in maintenance is roughly what I've gained in equity, but that is a very coarse measure and factors such as inflation can be a lot larger and so mask any retrievable result.

A point to bear in mind is that both the renter and the house-owner are using their money to buy a place to live. Some of that investment is in being able to enjoy that living space and many people would be happier if they approached change from that perspective – what you might do that causes you to enjoy life at home more. If you spend long periods not-at-home, perhaps you don't need to own, or to own something small ('convenient'). Do read [3] and [4].

DJS 20210907

[1] https://www.theguardian.com/business/2021/aug/18/Uk-house-prices-rise-at-fastest-rate-since-2004

[2] https://pearsonblog.campaignserver.co.uk/tag/house-price-inflation/

[3] https://www.investopedia.com/financial-edge/1112/reasons-renting-is-better-than-buying.aspx

[5] https://www.allagents.co.uk/house-prices-adjusted/

[6] Found while writing 372 - corruption, this: http://www.transparency.org.uk/sites/default/files/pdf/publications/House%20of%20Cards%20-%20Transparency%20International%20UK%20%28web%29.pdf I suggest reading at least the recommendations, pp8-11

Between January 2010 and March 2020:

• Political parties, their members, and other campaigns accepted donations totalling £742 million.

• Over 10%of all political donations during this period came from individuals and companies related to substantial property interests (£75.1 million).

• 80% of property related donations by value (£60.8 million) went to the Conservative Party.

• Property related contributions accounted for over a fifth of the Conservative Party’s reportable donations.

• Large property related donations accounted for 1 in 10 pounds of the Conservative Party HQ’s income between 2015 and 2019.

Yes, this is a report by people with vested interest in writing in criticism of the government (and that turns out to be the Tories often). When one (the authors) look at the available evidence, it is clear that while ministers do listen, they don't listen in any sense evenly, as the monied have access and the disadvantaged do not. For example, tenants. Do read this report, which is easy to agree with. I might point to the parallel situation with the media, who are required to exhibit 'balance' in their reporting (the BBC especially comes in for criticism). It looks to me as though that very same criticism could be applied with greater precision to ministers and, by extension to MPs. If they listen to one side, why are they not finding other sides of the same problem to listen to?